Almost every year, changes are made to the set of rules that govern how bankruptcy cases are managed — the Federal Rules of Bankruptcy Procedure. The changes address issues identified by an Advisory Committee made up of federal judges, bankruptcy attorneys, and others. Often there are revisions to the official bankruptcy forms as well.

One Little Rule Amendment? This year’s amendments impact only one rule, Federal Rule of Bankruptcy Procedure 1007. On the surface, the change is only a small revision to a reference to one of the official bankruptcy schedules. A link to a copy of the amendment, including the transmittal correspondence and a clean and redline version, can be found using the link in this sentence (and if you keep reading you will get the amendments to the Federal Rules of Civil Procedure as a bonus).

Big Changes Are Coming To The Bankruptcy Forms. Don’t let the minor rule amendment fool you. As one presidential candidate these days might put it, the changes coming to the official bankruptcy forms are “huge.”

- As part of a modernizing of the official forms, virtually every bankruptcy form is being substantially revised.

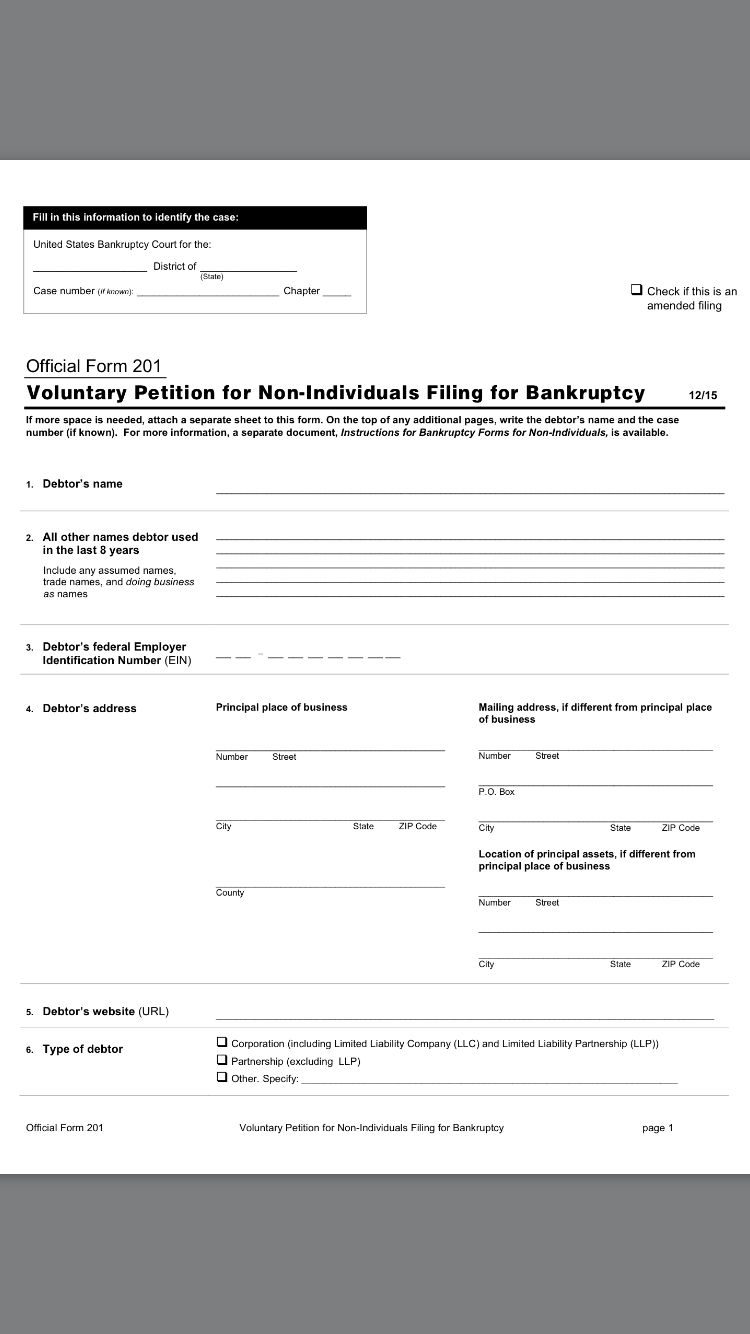

- Many forms, including the bankruptcy petition, list of 20 largest creditors, bankruptcy schedules, and statement of financial affairs, will now have customized versions for cases involving individual and non-individual debtors. The non-individual voluntary petition form pictured at the beginning of this post gives you an idea of how different the new forms look.

- Going forward, business bankruptcy cases filed by corporations, LLCs, and partnerships will use a set of forms designed specifically for businesses instead of having to respond to questions meant for individuals.

- The numbering system for the official bankruptcy forms is also changing. For example, forms bearing numbers in the 100 sequence will be reserved for individual debtors while those in the 200 sequence will apply to non-individual and business debtors.

Read All About It: Access The Revised Bankruptcy Forms. The U.S. Courts system has made the revised bankruptcy forms available now so you can get ready for the changes.

- Follow the link in this sentence for a PDF format of the revised forms with useful PDF bookmarks that you can access if you save the PDF. This document includes both the revised forms and accompanying official Advisory Committee notes.

- Another set of revised forms, known as the Director’s Bankruptcy Forms, used more by the courts themselves, is also available by following the link in this sentence.

- Click on the link that follows for a handy cross-reference conversion chart showing the old form numbers and names side-by-side with the new ones for individual and non-individual debtors.

- Finally, use the link that follows for a helpful information page prepared by the U.S. Bankruptcy Court for the Central District of California about the new forms, complete with an overview video.

Get Ready. These major changes go into effect December 1st so bankruptcy attorneys and others should take the time now to review the new forms and get ready to use them.